Money•5 min read

The Federal Reserve Has Spent Decades Relying on Surveys and Futures. A Betting Market Just Beat Them Both

Since 2022, the Federal Reserve convenes eight meetings a year to decide the price of money. At each of those meetings, the prediction market Kalshi correctly guessed the result the day before with a perfect record, something neither surveys of professionals nor rate futures managed to match. This isn't claimed by a crypto evangelist or a platform executive. The Fed itself says it.

On February 19, the Federal Reserve's Division of Monetary Affairs published the working paper "Kalshi and the Rise of Macro Markets" in its FEDS series. Its authors, Fed economist Anthony Diercks alongside Jared Dean Katz of Northwestern and Jonathan Wright of Johns Hopkins and the NBER,analyzed Kalshi's contracts on interest rates, inflation, unemployment, and GDP against traditional instruments: the Bloomberg Consensus, the Survey of Market Expectations from the NY Fed, and federal funds effective rate futures. The results show these markets generate well-calibrated, rapidly updating density forecasts of important economic variables, including several for which no alternative exists.

The concrete figures should make more than one institutionally housed economist uncomfortable. For FOMC decisions, Kalshi performs on par with professional forecasters when projecting 150 days out. But as the date approaches, the platform surpasses futures in a statistically significant way. On core inflation, Kalshi's results are comparable to the Bloomberg consensus. On headline inflation, the platform's median and mode achieve a statistically significant improvement over that same consensus. In the paper's own words: "Kalshi forecasts for the federal funds rate and CPI offer statistically significant improvements over futures and professional forecasters, and they do so with complete and continuously updating distributions rather than infrequent point estimates."

There's something here that goes beyond precision. Traditional instruments, surveys, futures,have a structural problem: they are snapshots. The Bloomberg Consensus updates from time to time; the Survey of Market Expectations, every six weeks. Kalshi trades second by second. While conventional surveys offer only point estimates, Kalshi's contracts, structured as Arrow-Debreu securities, allow for the construction of a complete risk-neutral probability density. This means analysts can observe tail risks, asymmetries, and variance, not just the central forecast. In an environment where a surprise in CPI data moves markets in minutes, the difference between "once a month" and "in real-time" isn't trivial. It's everything.

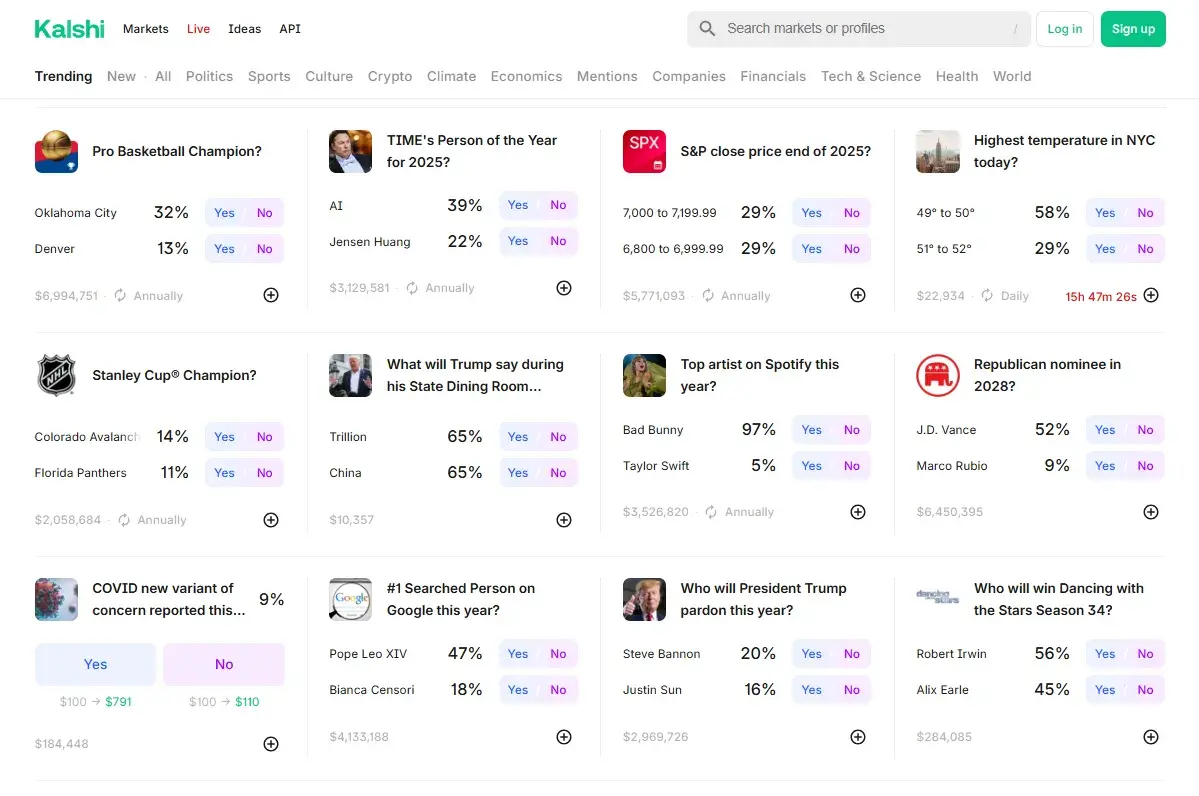

The mechanism explaining this performance isn't mysterious. Anyone trading on Kalshi puts their own money on every contract. There is no zero cost of being wrong, like there is in a survey. This retail participation is what distinguishes Kalshi from institutionally dominated markets, and part of the added value comes precisely from that broader, decentralized perspective. Trading volumes on the platform have grown to nearly 100 million contracts for a single FOMC meeting, with liquidity provided by firms like Susquehanna, Citadel, and Two Sigma. It's not exactly the digital casino its detractors wanted to see.

It's worth keeping in mind what this document is and what it isn't. The FEDS is a series of working papers circulated for discussion prior to formal peer review; the results express the authors' opinions and do not necessarily reflect the position of the Fed's Board of Governors. It's not a policy statement. And the study itself notes nuances: the Center for Economic Policy Research (CEPR) identified evidence of "favorite-longshot bias," the tendency of bettors to overestimate unlikely outcomes, which consistently appears in political, entertainment, and economic contracts. The report also warns of risk premium distortions and noisy estimates in contracts with low trading volume at the extremes of the distribution.

What changes with this paper is the board for regulatory debate. In 2025, Kalshi's monthly volumes surpassed $1.3 billion, nearly double Polymarket's; combined, both platforms had already executed $12 billion in trades during that fiscal year. Over the entire year, Kalshi cleared $43.1 billion, though more than 90% corresponded to sports contracts tied to its integration with Robinhood,while Polymarket closed 2025 with $33.4 billion. These are not niche volumes. They are the volumes of an asset class that is taking root.

The problem is that "taking root" in the United States comes with a considerable legal price tag. While Kalshi won in Nevada and New Jersey arguing that federal CFTC regulation preempts state gambling laws, a federal judge in Maryland rejected that thesis, and in January 2026 a Massachusetts court issued a preliminary injunction banning Kalshi from allowing state users to bet on sports contracts without a local license. The judicial map is a mosaic of contradictory decisions. The narrative "we are financial derivatives, not bets" works in some courts and not in others.

The new CFTC chairman, Michael Selig, confirmed in December 2025, withdrew both the 2024 proposed rule that would have banned political and sports contracts and the 2025 advisory warning registrants about those contracts. His position is clear: the CFTC claims exclusive jurisdiction over these markets and wants to be their sole regulator. The states view it differently.

The American Gaming Association has spent months lobbying against prediction markets. In the Fed's study, a spokesperson for the Coalition for Prediction Markets was unavailable for comment, and the AGA did not respond to a request for comment. A striking silence for an organization that typically doesn't hold back on statements when it perceives a competitive threat.

Prediction markets have spent years being treated as a curious experiment at the intersection of cryptocurrency and behavioral finance. The Fed report doesn't turn them into monetary policy instruments overnight, its own authors are careful about that,but it does make it harder to dismiss them as mere speculative entertainment. Kalshi correctly predicted the 50-basis-point cut in September 2024 when professional forecasters were divided. Futures failed. Consensus failed.

The question left hovering isn't methodological. It's political. If a market where any citizen with $50 can bet systematically produces better forecasts than the models of institutions with million-dollar budgets and decades of academic credentials, someone has to explain why that isn't legitimate. Until now, the answer has been jurisdictional. But jurisdictions can also be reformed.

Sources

- Federal Reserve – Kalshi and the Rise of Macro Markets (FEDS)

- Axios – Kalshi prediction market data earns vote of confidence

- Fortune – Kalshi maintains 'perfect forecast record'

- Gizmodo – Federal Reserve Says Prediction Markets Are a Valuable Tool

- The Block – Prediction markets explode in 2025

- Corporate Compliance Insights – CFTC Withdraws Proposed Rule

The most important news while you enjoy a cup of coffee.

Join our community. Get our exclusive weekly analysis before anyone else.

Related News

GlobalDinero

6 min read

Europe said no. Trump said he didn't need them. NATO has spent 75 years waiting for someone to explain the difference.

France, Germany, Spain, Italy and the United Kingdom refused to send ships to the Strait of Hormuz. Trump said he never needed them. Nobody yet knows whether either side really believes it.

TecnologíaDinero

5 min read

Meta lays off 16,000 people. Its stock rises 3%

Reuters confirmed plans to cut up to 20% of Meta's workforce. Wall Street celebrated the news with a 3% surge. In 2026, AI already justifies 55,775 layoffs in the tech sector.

Dinero

6 min read

Congress gave the casino industry what it asked for. Then added the fine print.

The same law that modernizes the reporting threshold on slot machines limits loss deductions to 90%, generating taxable income for gamblers who end the year in the red.